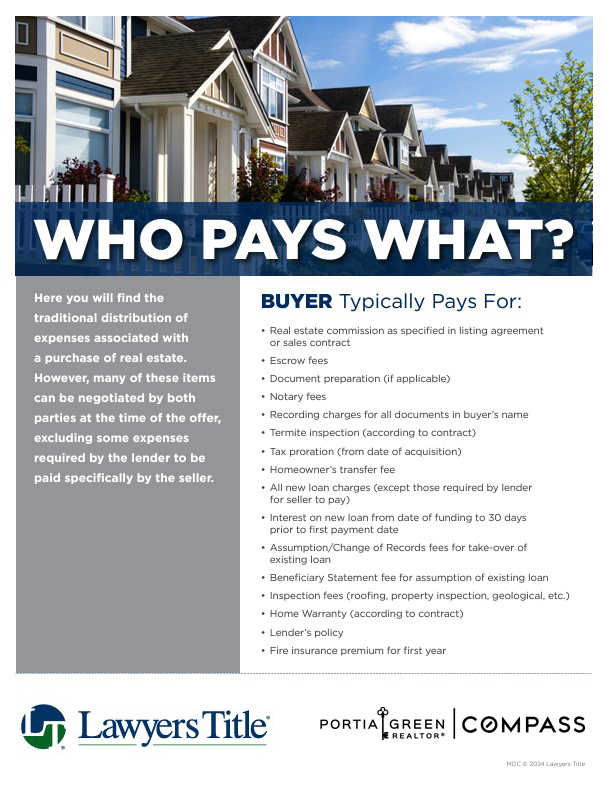

• Buyer Closing Costs Explained •

If you’re planning to purchase a piece of San Diego real estate, there’s more to consider than just the big price tag on the property. One often overlooked aspect of buying a house in San Diego are the closing costs, which can sneak up on you if you’re not prepared. Before you get too caught up in the excitement of your new San Diego address, let’s break down what you need to know about these extra expenses.

What Are Closing Costs for Homebuyers

When you buy a house in San Diego, the mortgage and down payment aren’t the only expenses to consider. Closing costs are a collection of fees that are due when you finalize your home loan. These fees cover everything from escrow payment and broker compensation to deed recording costs and loan-related charges, all of which can vary depending on the specifics of your transaction.

Here’s a detailed breakdown all about paying closing costs on your San Diego mortgage.

Different Types of Closing Costs Explained

Every real estate transaction will differ on exact amounts, but in general, you can expect to encounter the following types of closing costs depending on the type of property you buy and which mortgage you use:

1. Upfront Costs

These overhead costs are paid upfront, out of pocket, to cover things like home inspections and appraisals that are key to buying any house in San Diego with a mortgage involved. Your home inspection checks out the property condition and flags any issues before you finalize the purchase, while an appraisal figures out the home’s market value and is required by lenders to make sure the loan amount is right. These costs are important for a smooth buying process, so be sure to include them in your budget.

2. Escrow Fees

These fees take care of the legal side of things like holding deposits, dispersing the funds, and making sure everyone sticks to the Agreement. Escrow fees make sure the transaction goes smoothly, so there are no surprises at closing. They also ensure that all the necessary forms and documents are properly filled out and compliant with the law. The Buyer and Seller may share these costs, depending on what’s been agreed to in the Offer. It’s a small price to pay for the peace of mind that everything is handled correctly.

6. State & Local Fees

State and local fees in your closing costs include things like deed processing and recording fees, which are needed to officially record your property purchase. If your new home is in a Home Owner’s Association (HOA) community, you’ll also need to budget for prorated HOA fees. These costs can vary based on where you’re buying in San Diego County and the property itself, so it’s smart to check them out and factor them into your budget.

7. VA Funding Fee

The VA funding fee is a one-time payment made to the VA when you open a new VA loan. It can be paid upfront at closing or financed into your loan and ranges between 0.5% and 3.6% of the loan amount. Your individual cost may vary based on your down payment amount, loan type, and service status. Some types of VA loans have a higher funding fee if you’ve used your VA loan benefit before. On VA purchase and construction loans, making a larger down payment is the best way to lower your VA funding fee.

8. FHA Funding Fee

The Up-Front Mortgage Insurance Premium (UFMIP) is a one-time payment made at closing for FHA loans, designed to protect the Lender in case of default. This fee, usually 1.75% of the loan amount, is added to your mortgage balance and can often be rolled into the loan itself. It helps keep FHA loans accessible for buyers with lower down payments. Understanding UFMIP can help you budget more effectively for your new home purchase.

9. Flood Determination

Flood determination checks if your new home is in a flood zone. This usually costs a few hundred dollars and covers the review of flood maps and insurance needs. If your home is in a flood zone, you’ll need to get flood insurance for the life of the loan. Knowing about flood determination helps you spot potential risks and make smart decisions to protect your home.

10. Fire Determination

Fire risk determines whether your new home is at risk for fires. This fee, also a few hundred dollars, includes checking fire hazard maps and figuring out insurance requirements. If your home is in a high-risk area, you’ll need to get fire insurance to cover it. Understanding fire risk can help you avoid surprises and make better choices for protecting your property.

Who Pays the Closing Costs in San Diego?

Many people assume that the Buyer is solely responsible for closing costs, but that’s not always the case. Both the Buyer and the Seller often share these expenses. For instance, the Seller typically covers title insurance, county transfer tax, and can opt to cover real estate broker compensation while the Buyer handles mortgage-related fees, prorated property taxes, and home insurance. However, these costs are negotiable and can be factored into the Purchase Agreement.

How Much Are San Diego Closing Costs?

In San Diego, closing costs for Buyers generally range from 1% to 3% of the total purchase price. So, on a $1,000,000 home, you could be looking at anywhere from $10,000 to $30,000. It’s important to budget for these costs early on, so you’re not caught off guard at the last minute. Ask your Lender if you’ll need an additional mortgage reserve outside of the closing costs and down payments.

You have options for paying these costs: you can either pay them upfront as a one-time expense at closing, or you might be able to roll them into your mortgage. Just keep in mind that if you choose to finance your closing costs, you’ll be paying interest on them over the term of your loan.

The Bottom Line: Plan Ahead

Understanding closing costs is a big part of buying real estate in San Diego. While it’s easy to get excited about your new property, don’t let the closing costs sneak up on you. This breakdown of closing costs is thorough and covers the main charges that San Diego homebuyers should anticipate.

From escrow fees and prorated property taxes to loan origination fees and county surcharges, these expenses are an essential part of the San Diego homebuying process. Budget for them ahead of time and know what to expect, so you can ensure a smoother, stress-free closing.

Sources:

https://www.bankrate.com/real-estate/closing-costs-in-california/

https://www.rocketmortgage.com/learn/closing-costs

https://www.nerdwallet.com/article/mortgages/closing-costs-mortgage-fees-explained

https://www.investopedia.com/mortgage/mortgage-guide/closing-costs/

san diego home buyer closing costs, first time home buyer closing costs san diego, home buying closing cost assistance, what home buying closing costs are tax deductible, does a home buyer pay closing costs in san diego, what are closing costs on a house for a buyer, home buyer closing cost calculator, typical home buyer closing costs in san diego, cash home buyer closing costs, new construction home buyer closing costs, can a home buyer pay all closing costs, how much are closing costs for the buyer, does calhfa cover closing costs, redfin closing costs, redfin buyer closing cost calculator, zillow closing costs, zillow buyer closing cost calculator, opendoor closing costs, homes.com closing costs, bankrate closing costs, rocket mortgage closing costs, buyer closing cost breakdown, san diego home purchase closing costs, home buyer costs closing, first time home buyer grants closing costs, when purchasing a home who pays the closing costs, why do home buyers ask for closing costs, real estate buyer closing costs san diego, sd home closing costs, questions to ask before closing on a home, upfront home buying costs, va home loan closing costs, fha home loan closing costs, zero closing cost mortgage, san diego home buyer closing cost assistance

About The Author

Related Posts

2026 Strategy Shapes Results in San Diego Real Estate

• Strategic Momentum • San Diego real estate in 2026 rewards clear…

Increased Loan Limits in San Diego for 2026

• Mortgage Limits Rise • The Federal Housing Finance Agency (FHFA) recently…

The Housing Market Is Quietly Shifting in Parts of San Diego

• More Opportunity • San Diego real estate is entering a market…